SUMMARY

Since January 2024, the European Sustainability Reporting Directive (CSRD) has required listed companies with +500 employees and 50 million in sales to publish a report on their social and environmental impacts, as well as the impact of these issues on their business. These first reports, known as "double materiality" reports, were published in early 2025. Consulting firm BL évolution analyzed 85 reports from major French companies to understand which methodologies were favored and how CSRD structures their sustainability strategies. CSRD repositioned CSR as a strategic approach, questioning business models and value chains. While climate transition plans are relatively well integrated, only 28% of companies have detailed a plan ambitious enough to achieve their objectives, and less than 25% of companies have drawn up a biodiversity transition plan. 95% of companies have consulted their internal stakeholders, but only 67% have consulted external stakeholders, revealing a lack of understanding of their value chains.

A reform of the text, deemed too complex to implement, is currently under discussion at European level, but risks emptying the directive of its objectives, despite the fact that it places CSR issues at the heart of corporate strategy , identifying risks (as well as opportunities) more clearly and forcing dialogue between general management, finance and human resources with the CSR department.

Keywords: adaptation to climate change, biodiversity, value chain, climate, CSRD, sustainable development, duty of care, double materiality, companies, methodology, opportunities, risks, strategy, transition, France.

Illustration : © BL évolution

European Sustainability Reporting Directive (CSRD)

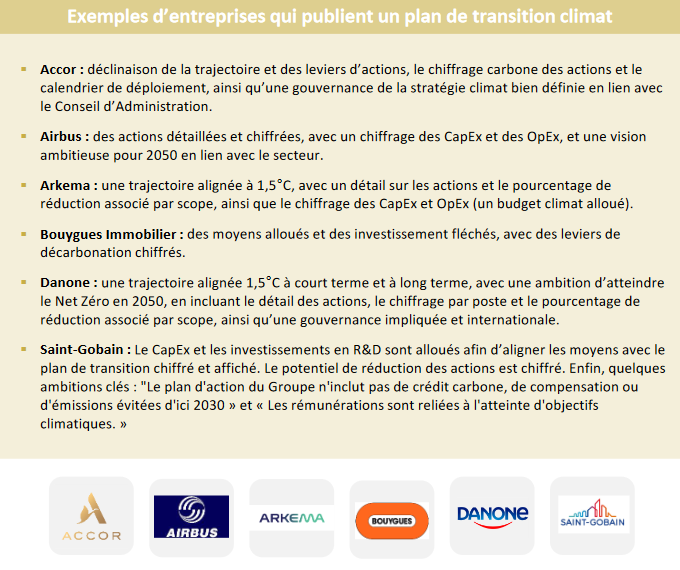

Examples of companies publishing a climate plan